| Lifetime Annuity and my 401k |

|

|

|

|

|

mikita21

New Poster

Cash: $ 0.45

Posts: 2

Joined: 10 Nov 2015

|

| Lifetime Annuity and my 401k |

|

|

Hello,

I have recently read a book by Tom Hegna, who writes at great length about the value of a lifetime income annuity. My question is this: is it a wise thing to withdraw from my 401k and purchase the lifetime income annuity? I am soon to be 63 and would plan to immediately draw from the lifetime income annuity. I am still working full-time and plan to do so until age 66.

Also, are there tax liabilities to withdrawing from my 401k like this?

I greatly appreciate any and all advice. Thank you in advance.

Ron

|

Tue Nov 10, 2015 3:13 am

Tue Nov 10, 2015 3:13 am |

|

|

oldguy

Senior Member

Cash: $ 751.85

Posts: 3656

Joined: 21 May 2006

Location: arizona

|

The annuity is under a lot of scrutiny the last few years, they have been oversold. "Trusted'" bankers take retired seniors to dinner and sell them inappropriate annuities. Congress has been looking at putting some limits on these 'over-anxious' sellers. Annuities are an exceptional deal for the SELLER, they make a huge and immediate sale. (When you buy an annuity, your money is gone, spent - you have only a contract that promises to pay forever). And the ongoing commissions pay the seller for your lifetime.

I avoid them, there are many better ways to use your money.

|

|

Tue Nov 10, 2015 3:53 pm |

|

|

mikita21

New Poster

Cash: $ 0.45

Posts: 2

Joined: 10 Nov 2015

|

Oldguy, I appreciate you! I was going to go spend $100k. Thank you so much for your counsel.

Ron

|

|

Tue Nov 10, 2015 4:06 pm |

|

|

littleroc02us

Moderator

Cash: $ 384.35

Posts: 1891

Joined: 09 Feb 2009

|

I am not of the age yet where these issues come into play, but from everything I've heard and read, it benefits the seller and not the investor. As Warren Buffet says: Risk comes from not knowing what you're doing. Annuities come with lots of fees and commissions that are profitable to the seller. Plus who wants to give up their hard earned money for a promise of a payback?

Risk comes from not knowing what you're doing. (Warren Buffet)

|

|

Tue Nov 10, 2015 4:08 pm |

|

|

PapaGeek

Contributing Member

Cash: $ 8.80

Posts: 41

Joined: 17 Jul 2014

Location: Maryland

|

|

|

|

I think the key to safe retirement is not to, as the old cliché says, put all of your eggs in one basket!

Our current plan would have 49% of our savings in IRA accounts, 28% in the cash value of our annuities, and 23% in our ROTH accounts. Our incomes would be 59% SS, 9% Pensions, 17% Annuities, and 15% Minimum Required Withdraws from our IRAs.

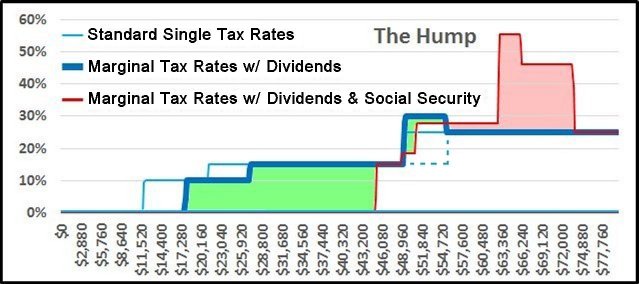

I think a more important aspect to your retirement planning is the avoidance of the tax humps that occur when your taxable income reaches the 25% level in retirement. At that point you are also being taxes on 85% of your Social Security benefits so a $100 withdraw from an IRA would result in $85 of your SSB being taxable and you would then pay 25% of $185 or $46.25 for each $100 withdraw, a 46.25% marginal bracket. If you are also getting income from dividends or long-term gains, the marginal Hump bracket can start out at the 55.5% level.

Proper planning before retirement might point out that what you need to do is to convert a portion of your traditional IRA to ROTH at the 25% level before retirement to avoid those high marginal brackets during retirement.

We were lucky enough to find this out a couple years before retirement and are currently in the process of doing yearly ROTH conversion at the tax levels we are comfortable with. Without the conversions we were going to be at the top end of the 15% bracket where any extra funds withdrawn would have been taxed at the hump levels. Doing the conversion will reduce the size of our Minimum Required Distributions from the traditional IRAs and also give us additional ROTH capital which can be taken out without any effect on our taxes.

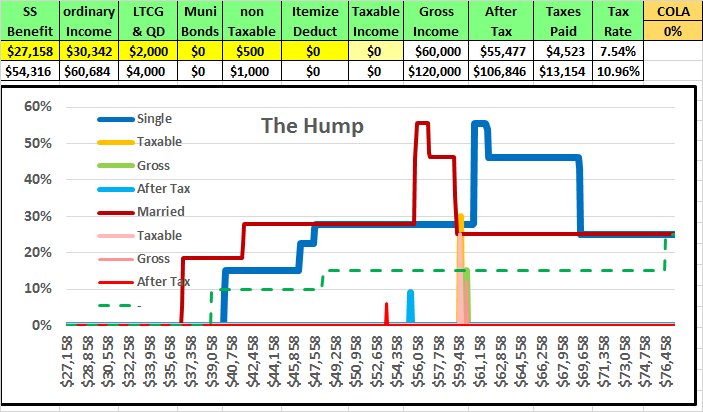

Here is a picture of what the Marginal Tax Brackets look like for single and married individuals. The scale is per capita gross income.

PS: These are not our numbers, they are only examples!

Last edited by PapaGeek on Mon Nov 16, 2015 2:21 pm; edited 2 times in total |

|

Sun Nov 15, 2015 1:26 pm |

|

|

oldguy

Senior Member

Cash: $ 751.85

Posts: 3656

Joined: 21 May 2006

Location: arizona

|

quote:

I think a more important aspect to your retirement planning is the avoidance of the tax humps that occur when your taxable income reaches the 25% level in retirement.

Not really, those 'humps' are only $3k to $8K wide, ie, the rates only apply to a small part of your gross - the 'real' tax rate for $120,000 gross is about 11%.

But converting several $100,000 of IRA to a Roth puts the conversion in a top rate - not a good plan.

|

|

Sun Nov 15, 2015 4:43 pm |

|

|

PapaGeek

Contributing Member

Cash: $ 8.80

Posts: 41

Joined: 17 Jul 2014

Location: Maryland

|

|

|

|

OldGuy,

Im not sure why you are saying Not really to the concept of paying 46.25% or 55.5% federal tax.

My issue is not what was my tax rate was for the entire $120,000 of income, but what is my next dollar of income going to cost me? At the 55.5% marginal level, paying 4.75% Maryland state tax plus 2.8% county tax brings me to 63.05%. If I need an extra $1,000 at that rate I have to withdraw $2,706.36 to pay the Federal the various tax grabbers $1,706.36 so I can keep $1,000 for myself.

If I am happily living at the start of the hump and the delayed taxation of my SSB has saved me thousands of dollars in taxes and Im enjoying that extra money, I dont want to give it back because my overall average isnt that high!

For a single individual getting about $30,000 in SSB and another $6,000 in dividends, the delayed taxation of Social Security leads to about a $4,000 annual delay in taxes paid. The Hump quickly gives back almost $2,750 of that savings over about $10,000 of gross income. The conversion of about $30,000 per year for 3 years, only about $100,000, not several times that much, can keep you in the 25% pre-retirement bracket. The minimum effect of this move saves you the 27.75% bracket in retirement so there will be a slight tax savings. If this can also save you an extra $1,000 or so each year the savings mount up.

Conversion to a ROTH has another major benefit, flexibility! When your retirement savings is in a Traditional IRA, there is a Minimum Required Distribution each year which can push you into tax brackets you want to avoid. You are not required to take anything out of a ROTH and when you do it has no effect on your taxes.

You are also correct when you talk about converting $100,000 per year. That will put you in the 28% or higher bracket before retirement, not the best way to go.

The width of the hump is totally dependent on the size of your Social Security benefit. If you retired at 62 taking the minimum benefits, you are correct, the hump might not even exist. If you work until 70 and take the max benefit your SSB could be almost $40,000 which would make your hump almost $20,000 wide.

Another situation for something like this might be a surviving spouse who goes on survivor benefits until the age of 70 and then switches to their own benefits at their max level.

The best plan is to take Black Friday each year to pr-plan your next years tax return. See how youre your taxable income is from the top of the 25% bracket, then convert that much from IRA to ROTH. If you want to maximize your conversion you will have to continuously re-calculate your state tax deductions which will lower your taxable income and let you convert more.

|

|

Sun Nov 15, 2015 7:04 pm |

|

|

craigd

Member

Cash: $ 3.25

Posts: 16

Joined: 14 Apr 2012

Location: Omaha, NE

|

Ron,

There is another option that has not been touched upon that I could review with you if you have free time in the near future.

After gathering some information from you, we can develop a strategy to navigate the complex financial landscape you are currently encountering.

|

|

Mon Nov 23, 2015 3:50 am |

|

|

christcorp

Preferred Member

Cash: $ 39.85

Posts: 199

Joined: 05 Mar 2015

Location: Wyoming

|

|

|

|

Personally, I think how you invest, and later withdraw, from savings, depends on one of two mindsets.

1. Live rich - and die poor?

2. Want to leave something for your heirs?

Not to be confused with having some sort of insurance or "taking care of your spouse" should something happen to you early.

I believe in the "live rich - die poor" category. I believe in planning to live a comfortable lifestyle, whatever you the individual define that as, and trying to work it out so there is little to nothing left when my time is up. When I help out my kids, financially, I want to do it for them when they are at an age that can use it. E.g. 30's when buying a home or having a family, grandkids, college, or whatever. When I'm 90, and they are 65, they should already be financially secure. "If I did my job right raising them". In case I get to the point where I have to wind up in a nursing home, assisted living, etc. I don't want to have to use all my savings for that because the government says I "can afford it".

Grant it, it is difficult to plan for when the end is near, but I figure that by the time I'm 80ish, my large expenditure days of traveling, toys, etc. are behind me, and I'll only need enough for month to month subsistence. I'd rather my kids get whatever I want them to have, when they are younger, so they too can save for retirement instead of living pay check to paycheck. Then again, if a person only has a little bit of money, and they are relying on social security, then they themselves are probably living on a fixed income, so leaving something for their heirs probably isn't part of the equation.

The way I see annuities, is that it's for the person who can't handle a lot of risk, they want a guaranteed income that they can budget until they die. Truthfully, anyone with an IRA, 401k, etc. can do exactly the same thing themselves. If you have any type of pension or retirement, along with social security, which I always recommend taking at the earliest time, you can manage your investments so you can withdraw a modest 4-5% from your investments to supplement your income for the next 30 years. Of course, a lot depends on how much you have. Even if you only have $100,000 in retirement, without any interest, you could take out $5000 a year for 20 years. That's about $400 a month. Maybe that can supplement your income, maybe not. With a modest retirement account, gaining a couple present interest, you can make that last about 30 or so years.

There's a lot of options. The bottom line is, are you wanting to leave something for heir, which I am against, "do that earlier when they can use it and you can afford it", or do you simply want to supplement your income from a retirement, pension, social security, etc.

|

|

Tue Nov 24, 2015 12:09 am |

|

|

PapaGeek

Contributing Member

Cash: $ 8.80

Posts: 41

Joined: 17 Jul 2014

Location: Maryland

|

|

|

|

quote:

Originally posted by oldguy

quote:

I think a more important aspect to your retirement planning is the avoidance of the tax humps that occur when your taxable income reaches the 25% level in retirement.

Not really, those 'humps' are only $3k to $8K wide, ie, the rates only apply to a small part of your gross - the 'real' tax rate for $120,000 gross is about 11%.

But converting several $100,000 of IRA to a Roth puts the conversion in a top rate - not a good plan.

Yes, it is true that the width of the hump is not super wide, but the taxes you pay in that hump are super high!

This illustration shows someone who is getting $30,000 in SS benefits and has $6,000 in annual dividend income.

At the $62,800 gross income level, just before the hump, they are paying $4,204 in federal tax.

At the $73,680 gross income level, just at the end of the hump, they are paying $9,521 in federal tax.

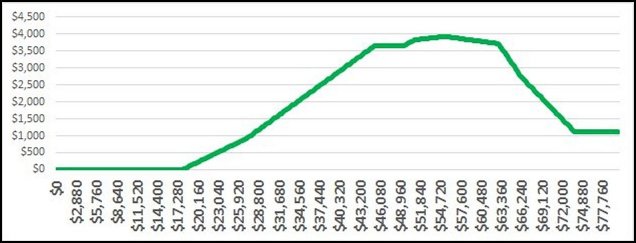

The hump was $10,880 wide, taxes paid in the hump were $5,316 and the overall effective tax rate in the hump was 48.86%. At the 25% level after the hump, an extra $10,880 would only result in a $2,720 tax increase. In the hump you are paying an extra $2,596.

Here is another way to look at the hump taxes.

The delayed taxation of your SS benefits results in a relatively large level of tax savings before the hump, then you have to give it back to the government while in the hump, why give it back?

If your planned retirement standard of living is in the 6 figure range, the effort needed to keep those tax savings is huge and not worth the effort. But if your planned retirement income level are in the upper 50s to lower 70s it is definitely worth the effort to at least look at the situation and see what can be done.

Yes, the conversion of SEVERAL $100,000 at once comes at a huge tax cost. But if your pre-retirement income level in around the $70,000 mark, your taxable income will be around the $60,000 mark and the top of the 25% bracket is around $90,000, so you could easily convert $30,000 a year at a tax level that would be equal to 25% level or slightly lower than the 27.75% level that you will most likely be paying during retirement.

Im not recommending that everyone should do things to avoid the hump. I am saying that everyone should be aware of the hump and where their personal retirement plans put them in relationship to it. To most it will not be a big deal and they can ignore what they see. But to some it can make a huge difference.

|

|

Tue Nov 24, 2015 9:07 am |

|

|

|